How US Opportunity Zones Really Work

tl;dr: Investors can dodge taxes by parking their capital gains in ~6,400 designated low-income census tracts.

Idea

After the 2008 financial crisis, investors retreated from risky markets (e.g. distressed towns) and chased trusted collateral (e.g. coastal real estate). Affluent communities recovered while poor towns starved of capital.

Changes in jobs/businesses by community prosperity quintile, 2011-2015, via EIG.

Meanwhile, US investors sat on trillions of dollars of unrealized capital gains. Selling a stock triggers taxes, so people held on for opportunities that (A) offset their realized capital gains and (B) make more money.

In 2015, EIG suggested waiving taxes for capital gains deployed into a capital-starved community, i.e. an "opportunity zone" (OZ).

The 2015 paper was co-authored by Kevin Hassett (Trump's Council of Economic Advisers chair) and Jared Bernstein (Biden's Council of Economic Advisers chair).

Deferring a capital gain typically only works when trading real estate for real estate (i.e. 1031 exchange). But with EIG's OZ proposal, you could defer a gain from any asset class (e.g. stocks, crypto, a whole business, collectibles) by rolling it into an OZ fund.

Law

Opportunity zones hit Congress in April 2016 as the Investing in Opportunity Act. It died in the Senate Finance Committee.

The bill was sponsored by Tim Scott (R-SC), Cory Booker (D-NJ), Pat Tiberi (R-OH), and Ron Kind (D-WI).

In December 2017, Congress folded the idea into the humongous Tax Cuts and Jobs Act, which became law.

Here's how it works for investors:

- If you take on a realized capital gain (e.g. you sell stock/crypto/equity/asset/etc.), you have 180 days to roll it into a Qualified Opportunity Fund (QOF). Anybody can create a self-certified QOF via IRS Form 8996. To qualify for benefits, the fund must keep 90% of its assets inside a designated zone.

- Whatever the QOF buys must be (A) built new or (B) substantially improved. For an existing building, the fund has 30 months to double its basis (i.e. spend as much fixing it up as it paid to buy it).

The whole OZ 1.0 clock runs to a fixed date: the deferred tax is due at the end of 2026 no matter when you bought in, so the pause is shorter the later you invested — about seven years for 2019 money, five for 2021.

Here's what you got for parking your gains:

- Deferred: Taxes on your contributed gains are deferred until 2026.

- Reduced: 10% of deferred gains were waived after 5 years (or 15% over 7 years).

- Rebased: Step-up basis to fair-market value at sale if held for ten years. The depreciation you deducted during the hold is not recaptured.

- Waived: Taxes on the fund's gains are waived entirely if held for ten years.

Bonus: A Qualified Opportunity Zone Business (QOZB), which keeps 70% of its tangible property in-zone, unlocks a 31-month "working-capital safe harbor" (i.e. it doesn't need to pay taxes on its unspent cash).

$100 long-term gain at 23.8% top rate, fund value doubling over ten years.

In early 2018, 31,680 low-income tracts (and ~9,450 contiguous neighbors) were eligible to become opportunity zones; each governor could nominate 25% of their State's eligible tracts. In June 2018, the US Treasury certified 8,764 tracts (including most of Puerto Rico). These designations were locked for 10 years with no mechanism to swap tracts.

Low-income tracts are defined by populations who (A) exceed 20% poverty or (B) fall below 80% of surrounding area's median family income.

Designated Opportunity Zone tracts per 100,000 residents, via CDFI.

Effects

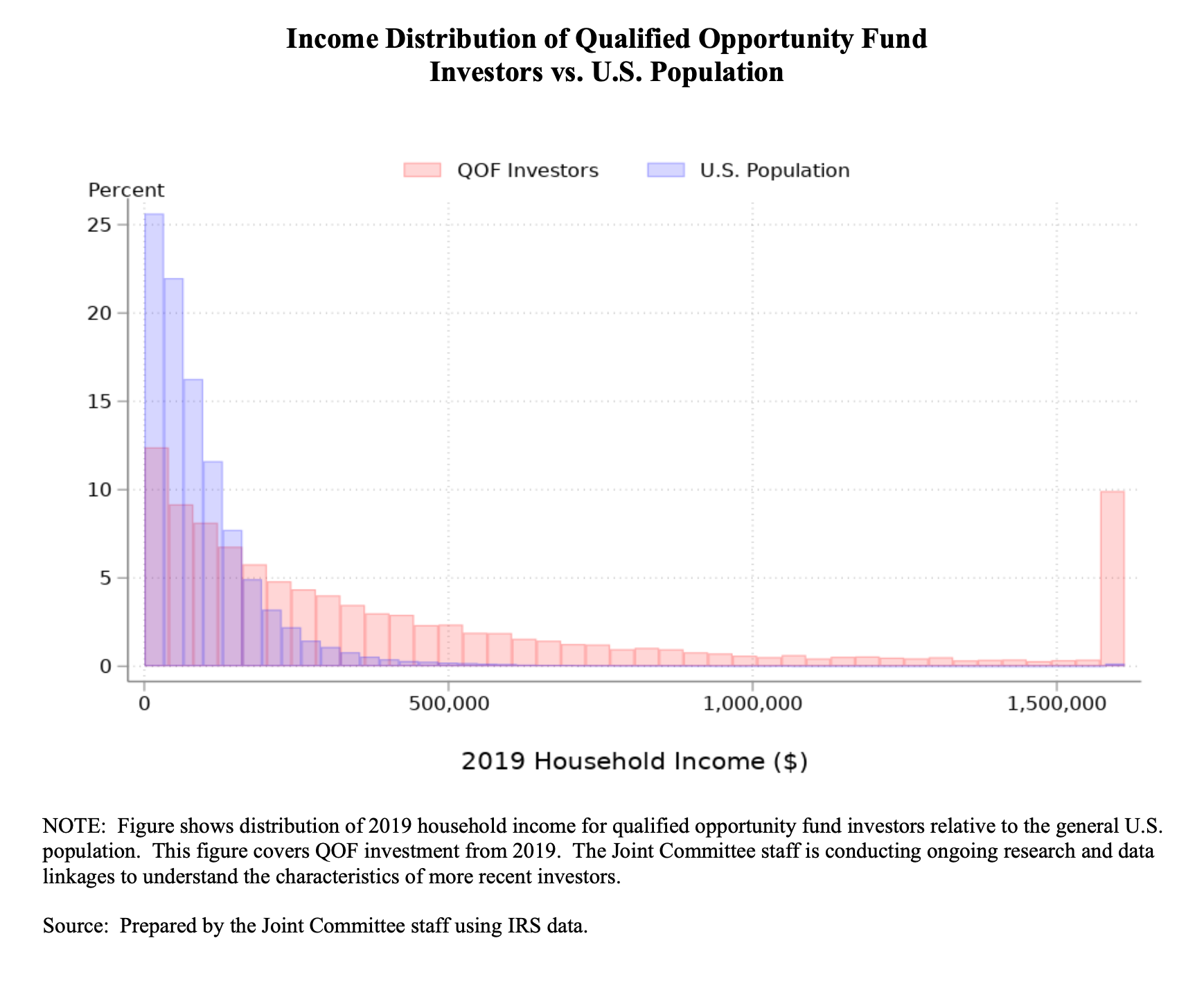

Opportunity zones lured in the billionaires. This should be no surprise — the investors with all the unrealized capital gains suddenly had a safer way to put their money back in the game. Well-designed incentives can entice people to trade their valuable stocks for distressed land.

The biggest OZ fund sponsors were conventional real-estate shops. Bridge Investment Group led with roughly $3.7 billion raised, followed by CIM Group (~$2.3B), Griffin Capital (~$1.6B), and Cantor Fitzgerald (~$1.1B).

Cumulative equity in opportunity funds, via JCT.

But opportunity zones specifically reward holding appreciating assets in a fixed place for ten years. Real estate naturally fits these criteria, but buildings are not necessarily businesses.

Share of investment by sector, via JCT.

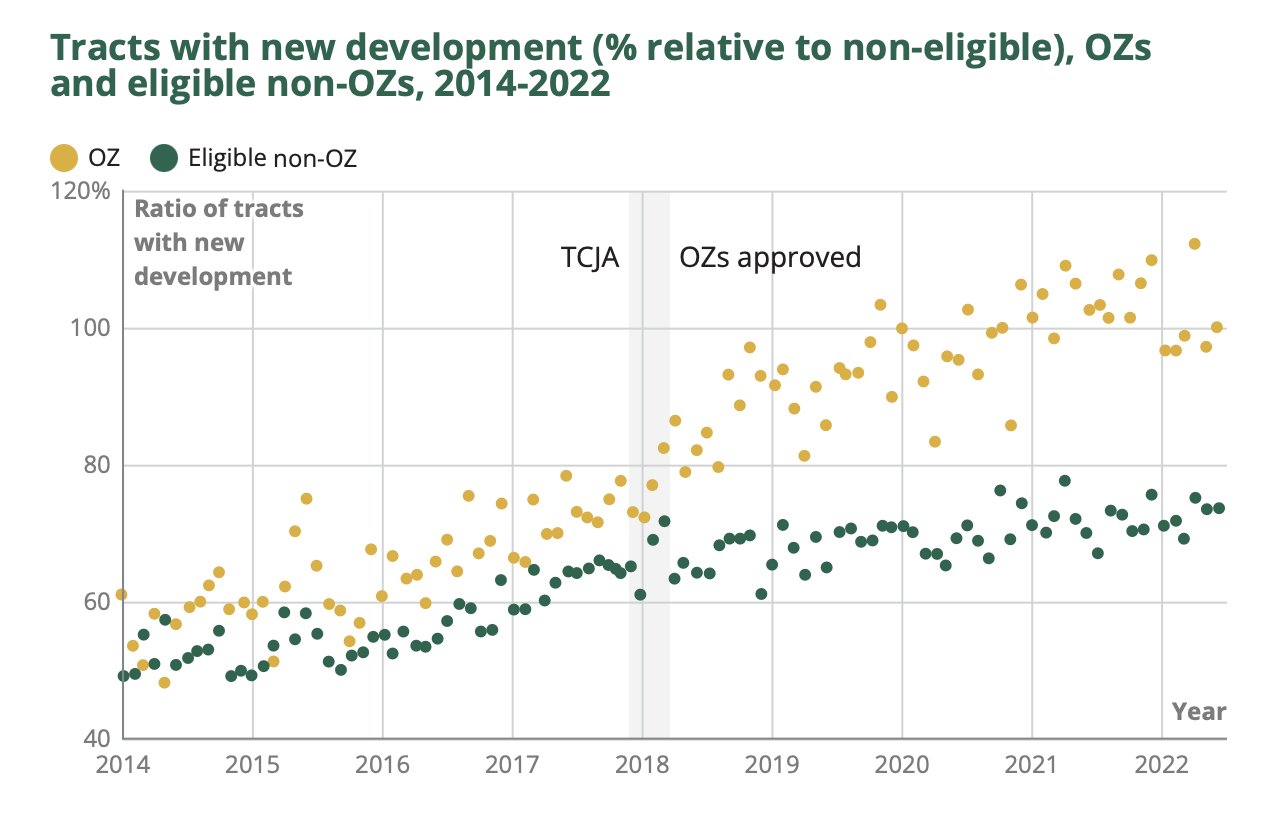

Even with tax perks, ten years is a long shadow. Of the eligible tracts that were nominated, most received no investment whatsoever. OZ funds ate low-hanging fruit. Money flowed into tracts with already appreciating land values (or intrinsic strategic value).

Distribution of QOZ property investment, US Treasury.

5% of a State's designated zones could bypass the low-income threshold if (A) they shared borders with a designated low-income tract and (B) their median family income did not exceed 125% of the poorer tract's.

Reporting requirements were stripped from the original law, so investigative journalists filled gaps for the program's first two years. The New York Times traced how a Nevada tract (Tesla's Gigafactory) with 7.5% poverty made the list when the Treasury overruled its own staff after a Milken Institute event. ProPublica documented how a Baltimore $233M waterfront megaproject (owned by Under Armour's Kevin Plank) qualified via a digital-mapping artifact.

But the "contiguous loophole" was not exploited as much as expected. Only 230 non-low-income tracts (2.6% of the 5% threshold) were designated.

Averages of tract-median values, via Urban Institute.

Of course some investors abused OZ incentives, but money generally flowed into low-income tracts as intended. Someday we may know whether those private investments actually outweigh lost tax revenue.

Extension

OZ 1.0 was set to expire on December 31, 2026.

But the One Big Beautiful Bill made opportunity zones permanent in July 2025. OZ 2.0 follows the same playbook with stricter eligibility requirements (and zero contiguous tract provisions). Only 60% of OZ 1.0 tracts are fully eligible for OZ 2.0.

Tracts' median family income threshold was reduced to 70% (prev. 80%) of the State's median (or surrounding metro area).

Starting January 2027, here's what you get in OZ 2.0:

- Deferred: Taxes on your contributed gains are deferred for 5 years.

- Reduced: 10% of deferred gains forgiven after 5-year hold (30% for rural QROFs).

- Rebased: Step-up basis to fair-market value at sale if held for ten years. The depreciation you deducted during the hold is not recaptured. OZ 2.0 automatically rebases to FMV at year 30.

- Waived: Taxes on the fund's gains are waived entirely if held for ten years.